Background

I am busy writing "The Simple Guide to Investing for your Child's Education". It is a no BS guide for South African parents. If you want to be notified once it is released please sign up at the bottom of this page.

The post below is an excerpt from the guide.

Tax Free Savings Accounts and Twitter 🙋

“I am looking to save money for my young child's education. University fees are ridiculously high. I know it is a good idea to start saving now. I heard about these Tax Free Savings Accounts in the news.

Should I open a Tax Free Savings Account in my child’s name to fund their tertiary education?”

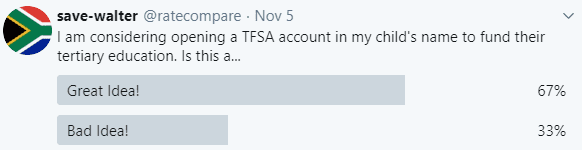

Great question. When in doubt, turn to Twitter. So lets run a Twitter poll. Drum roll, please... 🥁🥁🥁

Awesome. 67% of people voted for "Great Idea!". Decision made. Thanks Twitter. So we will go with group wisdom here. Me thinks?

Here is what you should do instead!!

No. No. No. Do not open a TFSA account in child's name to fund their tertiary education! You would be royally screwing them over financially. It is the equivalent of giving them a great pile of cash, only to steal their kidneys and selling them on the black market and then burning the proceeds. “What? That is brutal and does not make any sense!”, I hear you saying. Exactly, that sentence is just as non-sensical as you opening a TFSA account in your child’s name and withdrawing the funds to pay for tertiary fees. Brutal!

Simple rule. Print this out. Hang it next to your mirror and read this simple rule out loud every morning:

"I will not sell my child’s kidneys on the black market and I will not open a TFSA account to fund their tertiary education".

A Horror Story Featuring You

If the above kidney selling story does not convince you, then this section is for you. Hold onto your horses - here we go.

This story features you, the parent. The one who wanted to do well but instead did the opposite. Like all stories, we start at the beginning. A happy beginning. Unlike the happy beginning, however, the end is not. Yet I am jumping ahead...

The Happy Beginning

“It’s a girl!” - the doctor shouts. Long painful hours are instantly replaced with an overwhelming feeling of joy, pride and love. You have just witnessed a true miracle. The birth of your child. Your first-born. Yet there is another feeling nagging at you. An immense feeling of responsibility towards this helpless being.

You take a deep breath. As you exhale, you notice a big blue poster stuck to one of the maternity hospital walls. Bold white letters stare back at you. “Santram Education Plan - Investing in an education plan is one way of ensuring your child gets the best tertiary education possible. Terms & Conditions apply: Santram may or may not charge you exorbitant fees if your child is deemed human” (Please note that all names - including brand names - have been artificially changed for this story 😉 ).

Wow. You generally do not consider yourself a sucker for signs, but this sure feels like divine intervention. With this newfound purpose, you decide to start saving for your newborn’s education right then and there. After doing some research and asking your Twitter friends, you open a Tax Free Savings Account in your child’s name. At the ripe old age of two months, you start contributing a healthy R 1500 per month. Being uber-responsible you decide to increase the monthly contributions, by 6% - in line with inflation - every year.

You pat yourself on the back and mutter “Good parent. Good”.

The Mistake

Fast forward to the time your daughter reaches the age of seventeen. You are quite a bit older but the extra grey hairs suit you and you are just as good looking - if not better - than you were all those seventeen years ago. You also stuck to your monthly contributions throughout the years. These now amount to the full lifetime contribution of R500 000. The maximum you are allowed to contribute to a TFSA. The underlying investments were invested in the JSE - our local stock market - which experienced some turbulent times but still provided an average 10% annual return Well above inflation You proudly stare at the figure in the TFSA, which now amounts to R1.01m. “One million Rand. This will cover all of my child’s tuition fees, accommodation and meals as well as the expensive trips back home! It will even last for her Honours and Masters degree”. You proceed to cash in all those funds and dutifully pay for your daughter’s tuition fees out of her TFSA Account.

Fast forward another ten years. Your daughter is twenty-seven and has landed a great job thanks to a good degree. Unfortunately, unlike her peers, she is unable to contribute to the government-endorsed Tax-Free Savings Account since the maximum life-time contributions of R500 000 were reached and exhausted all those years ago. Oh well - it’s not that much of a biggie, she did get a fully paid education all funded by the good parent - aka you.

The End

Fast forward another thirty years. Your daughter is nearing retirement at age 57. She was hoping to retire at age 60 like her friends. There is only one issue. Unlike her friends, who all put R2750 per month into a TFSA account between the ages of 24 to 39 and can now enjoy the fruits of those savings - all tax-free - your daughter needs to continue slaving away. Years of tax free compound growth and the future tax free income have resulted in her friends being happy, early retirees.

Then came the holidays & the T-Shirts. You see unlike Living Annuities, Tax-Free Savings accounts do not place any restrictions on you in terms of when and how much you withdraw - so her friends chose to enjoy the Caribbean islands for two weeks “to just relax and enjoy sipping on some Mojitos on its white beaches”. They also had T-Shirts made - “This was paid by SARS”. Your daughter, unfortunately, did not get one.

'Old' You Reflects

By this time, you are in an old age home. In between your favourite TV episodes of “My Cruise Ship Tour”, you also get a lot of time to reflect and think. And finally, it dawns on you. You took away a great savings vehicle from your daughter all those years ago when you chose to open a TFSA account in her name to fund her tertiary education. You realise that the benefits of a tax-free savings accounts only materialise once you become a tax-paying citizen. Whilst your daughter was at university, she did not have a job and was effectively at a zero marginal tax rate. Thus those tax-free benefits which SARS preciously handed out via the introduction of a TFSA, were not realised when you cashed in those savings. Not only did your daughter not benefit from any of tax-free giveaways from SARS, but she also missed out on getting to experience the sweet-spot which a TFSA can provide. If you contribute early and then hold onto a TFSA for the long-term - as her friends did - you benefit from years of compound, tax-free growth and will get to retire early and enjoy long walks at the beach.

“Bad. Bad parenting” you mutter to yourself.

The Top 5 Take Aways

Do not open a Tax Free Savings Account (TFSA) in your child's name to fund their education

TFSAs are great tax savings vehicles set up by our Government.

The tax free benefits of TFSAs only start kicking in once you are a tax paying citizen.

Withdrawals out of TFSAs are precious as you cannot top them up again. You are limited to life-time R 500 000 contribution

The real juicy benefits of TFSA - aka the sweet spot - kick in if you hold on for the longer term. Ideally until retirement.